The Easy Method of Determining Your Life Insurance Requirements is

Life insurance is a financial tool that can help individuals accomplish a variety of financial goals. Most commonly, life insurance provides for dependent family members in case of premature death. Life insurance can also be used to fund certain goals, such as a child or grandchild's future college expenses.

As an estate planning tool, life insurance can help pay federal and state estate taxes, as well as estate settlement costs. The ultimate gift can be given using life insurance by transferring wealth between generations and making charitable bequests.

In order to properly utilize this powerful tool to help an individual reach his/her financial goals, it is important to understand the methods for determining how much insurance is appropriate in a given situation. Because each person's situation is unique, each case must be approached with the individual's goals and objectives as the driving force behind assessing the insurance need. There are three popular ways to calculate an individual's insurance need.

1. Rule-of-Thumb Approach

This method of calculating an individual's insurance need is the most basic. It focuses on how much insurance coverage a family needs to replace a breadwinner's earnings while maintaining their standard of living. The general idea is that insuring for an amount equaling six-to-eight times an individual's annual salary will provide adequate coverage in most situations. A couple of variations to this approach can be used that may provide a more accurate calculation:

- Multiply the gross income of the breadwinner by five, then add in mortgage, other debts, final expenses, and any special funding needs (i.e., college expenses).

- Spend an amount on annual insurance premiums equal to 6% of the breadwinner's gross income plus another 1% for each dependent.

While this approach can provide a basic estimate of the insurance need, it does not take into account individual circumstances, such as the insured person's age, the age of the dependents, or whether the home is a one or two income household.

2. Income Replacement Approach

This approach uses the human value life concept to measure an individual's insurance need. The method states that the economic value of a life is the present value of the future earnings potential of that person.

The amount of insurance needed will equal how much the insured person will earn until retirement. This amount is based on a number of factors including current after-tax income, income growth rates, an after-tax discount rate (or expected future investment returns), and the remaining number of years the insured person is expected to work.

There are several potential adjustments to an individual's income to consider to calculate an accurate insurance need:

- The current income value used should be adjusted downwards as self-maintenance expenses are not included in the portion of salary spent supporting the family. This means that any money spent on the insured will not be needed to support the family because the insured is deceased.

- The cost for insurance premiums is not used to support the family once the insured is deceased. Those premiums will no longer be paid and should be excluded from the annual income amount.

- The future income provided by social security survivor benefits should also be taken into account when calculating how much income is needed to maintain the family's current standard of living.

An income replacement approach will provide an insurance estimate based on the income of the insured that is spent on the family, taking into account income growth rates, discount rates, the working lifetime of the insured, and the insured's number of dependents.

3. Needs Approach

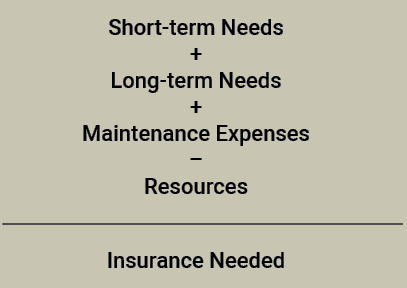

The needs approach is another simple formula that is used to calculate an individual's life insurance need based on several calculations.

- Sum all of the individual's short-term needs, which likely fall into three categories: final expenses (funeral, attorney, probate), outstanding debts (credit card, auto loan, college loans), and emergency expenses (medical, auto/home repairs).

- Calculate all of the individual's long-term debts and obligations, such as mortgage and college tuition expenses, using the future value of money equation.

- Calculate family maintenance expenses (i.e., living expenses), which include necessities such as food, clothing, utility bills, and transportation, using the future value of money equation.

- Calculate what resources an individual has to meet their needs. Resources include all available savings, stocks, bonds, mutual funds, and existing life insurance policies.

The remaining amount when resources are subtracted from income needs is the amount of life insurance an individual should consider. This number may be altered by eliminating any unnecessary expenses.

In general, this analysis should be done at least every three years, or when there is a major life event, like purchasing a home, the birth of a child, etc.

Life insurance may not be for every individual, but it can play an important role in the financial planning process when used appropriately. Each individual will have their own set of goals and priorities. By accurately calculating these needs and deciding which policy best suits them, one can help make sure those needs are met.

A financial planner or insurance expert can help guide someone considering a life insurance policy through the process of deciding how much insurance and what type of policy they will want, basing those calculations on family needs. Due to the complex tax treatment of insurance policies and their use in estate planning, it is important to consult qualified tax and legal professionals to ensure the policies selected are consistent with overall financial goals.

You can read more articles like this in our second edition of Prosper, our financial planning magazine. We address a diverse range of topics, including retirement planning, investing, estate planning, charitable giving, insurance, taxes, and so much more.

Request your copy >>

Consult with an attorney or a tax or financial advisor regarding your specific legal, tax, estate planning, or financial situation.

Source: https://www.manning-napier.com/insights/blogs/financial-planning/3-ways-to-determine-how-much-life-insurance-you-need

0 Response to "The Easy Method of Determining Your Life Insurance Requirements is"

Postar um comentário